The year 2021 gone by and speeded up the processes that many companies were trying to implement before and also shed light on some new challenges and opportunities. We have witnessed the wide range of technological breakthroughs, which let many players to optimize costs and implement new solutions. Today JuicyScore experts are eager to tell about the key fintech trends to watch in 2022.

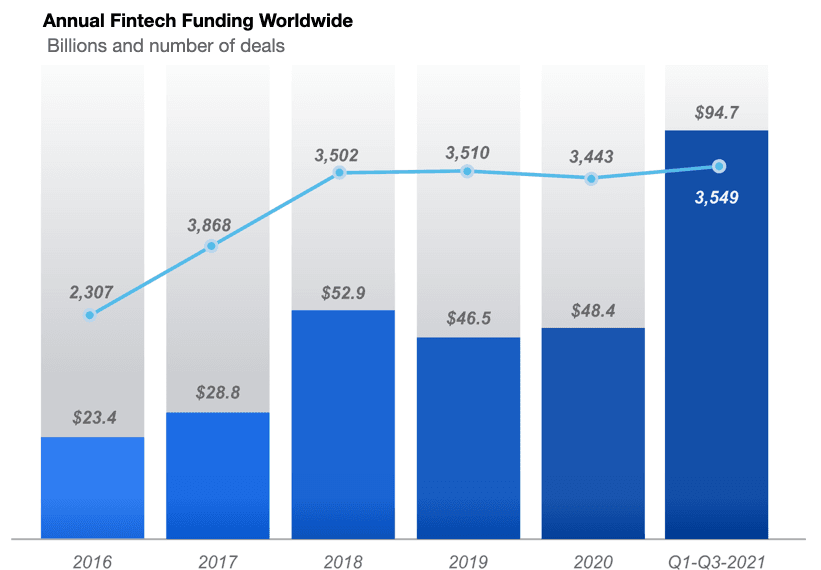

According to Insider Intelligence, during the first 3 quarters of 2021 fintech companies raised over 94 billion dollars, almost the same number as past two years combined. However many experts believe that many technological breakthroughs are yet to come. In the beginning of 2022 we can see that Fintech market growth is far from declining, this year fintech industry may astonish us all by new achievements.

Financial services trends and Web 3

Web 3.0 has attracted the attention of experts in recent years. Users are not only interacting with apps, but apps and devices also interact with each other, creating a more open and intelligent Internet. In addition, data in Web 3.0 is much more interconnected.

However, talking about Web 3.0 in the context of financial services, most people are referring to the next generation of the Internet, which will be decentralized and will run on a distributed infrastructure built on open standards (including blockchain), while the current version of the Internet relies heavily on various mediators, who also usually control the flow of information. Thanks to the extremely wide opportunities given by blockchain programming, with the use of smart contracts that allow to implement rather complex logic, even the most elaborate financial transactions and e-commerce can be implemented by means of Web 3.0.

In 2022 experts expect traditional financial institutions, financial service providers, and even some governments to test Web 3.0 technologies to improve and simplify financial service rendering. However they also expect that the regulatory framework will continue to evolve and adapt to circumstances where there are no mediators with registration or license obligations.

Development of new generation banking platforms may be reviewed as an example. In particular, a platform which provides compliance with regulations, security and issues instant loans. Also trading platforms based on blockchain technology are also being developed currently, which facilitate making payments abroad. Another example is distributed digital global ledgers through which financial institutions could provide every user with one’s own records and a user could have secure access to this information online.

Changes in workflow and labour management

The remote work format is already familiar to many online businesses. The consequences of the pandemic no longer seem so irrecoverable - the most successful companies have adapted to new conditions and are gradually developing new ways to organize workflow processes in order to make remote or hybrid work format more efficient.

Apart from that online companies are interested in changing the approaches to product development in order to achieve better results. In particular, ValOps/DevOps are replacing Agile, since DevOps and ValOps-commands reduce the product development time. At the same time, the high speed of development is also followed by sustainability and quality, so the companies’ management now rely not only on speed, but also on process automation.

Also, many online companies are coming to the conclusion that a reasonable approach to work-life balance, in particular, reducing the workweek from 5 to 4 days, maintaining the same scope of work, also motivates employees and attracts prospective ones.

Another trend is related to staff turnover - this lets to accomplish maximum efficiency and at the same time encourages workers to leverage their skills in order to achieve vertical growth. Also one of the consequences of this trend is a gradual increase in the pay gap between the "best" and "worst" employees.

The rise of global cloud and private networks

According to Statista, in 2021 50% of the volume of all the essential corporate data was stored in a cloud services. The amount of such services as well as the data volume are growing immensely because of online companies, which therefore expect to boost business agility. At the same time the pandemic has become some kind of a trigger for the trend increasing, for such services play a significant role in remote work organization. Many companies consider cloud services to be key factor of business development.

However it should be noted that the development of global private networks in the first place is related to the idea of secure and sustainable internet. Online companies are trying to rise the security and reliability of data storage.

Notably, speaking of the development of private networks the same trend is likely to happen at the national level in various countries. The global cloud private networks market size was estimated at $18.08 billion in 2020 and is expected to reach $75.64 billion by 2026 with a CAGR of 26.9%.

Further development of AI and ML technologies and regulation rules

Information is highly valuable resource in the 21th century. Its volume is growing every year and various methods are used to process these data arrays. Being a subtype of machine learning, DML’s (Deep Machine Learning) main feature is the use of machine learning methods and neural networks to solve real problems similar to human ones. DML searches for deep intermediate relationships between factors. Each element of the found dependence should be checked for stability and could be used to solve the problem of the next level - a particular hierarchy of attributes that were obtained by one or another statistical algorithm is built in the system, and each new layer has data about the previous one. From a practical point of view, to solve the top-level problem, an ensemble of models is used, each of which solves one of the problems below in the hierarchy. Related business tasks may include fraud / spam detection; speech / handwriting recognition; translation and imitation of many other human cognitive functions.

Artificial intelligence (AI-based) tools, which are actively used by fintech today, have already had a huge impact not only on the financial sector, but also on the whole world, they solve the problem of financial inclusion that has become very acute in recent years.

It does not take a Crystal ball to forecast that AI and DML technologies will continue their development. Growing trend for data collection and access regulation (both personal and user data) will inevitably affect data processing and data analysis methods which subsequently result into AI regulation. Why is it inevitable? Many algorithms both existing and under development require data collection for modelling and model renewal. In case this data has been collected without needed user permission it may impose risk up to full data usage restriction. That means that data processing algorithms and models based on such data will be also restricted. One of the ways to balance such risk may be found in preliminary data depersonalisation, generalisation or “roughing” before this data will be used for modelling and algorithms design. This approach will allow to comply with data owner rights even if it cause models worsening at the first stage. A spectacular example is endless discussions around Google Topics/ FLoC API.

Many experts say that in 2022 there will be a pressing need in regulating this area. Indeed, many companies continue to invest in AI and develop new methods without a solid legal foundation, large number of big companies have so far relied on the principles of self-regulation, which supposed to be more or less in line with the latest practices. Lack of AI regulation is not necessary a bad thing, as it gives companies more freedom to explore and test new AI features without constant pressure from regulator entities. However, currently there are no existing precedents as well as established approaches to legal regulation of this situation. The major frameworks will be adopted in the US and Europe in the second half of this year.

Quantum encryption and quantum computing

Assumptions that quantum technologies are coming around the corner seemed to many experts rather bald, however within the last 5-7 years everything changed completely. The basis of quantum technology is quantum particle (qubit), which can be in superposition or, in other words, maintain multiple possible states simultaneously, opposed to bits, which may store only a 1 or 0. Thus, quantum computing let us to make not sequential computing, but parallel, processing huge amount of data at the same time. Earlier experts believed that quantum computing can help us to solve such problems, which we can not define yet, however some projects already do exist - for example, giants like Google or Toshiba have already showed to the world the first prototypes of quantum computers. China, Europe and Russia also support similar projects.

What problems can be solved using quantum computing?

First of all quantum computing may be used in financial sector in order to solve optimization problems or quantum communication maintenance. The training of classical neural networks and artificial intelligence also needs optimization, in its turn, Machine learning complements this development.

In view of this trend, there is also a question related to information security methods. Most of the cyber defense infrastructures which are currently used, namely public-key cryptography, can soon be replaced with quantum cryptography, which will be based on quantum entanglement (if some bit of information has been seen by anyone who was not supposed to see it, the properties of such bit will change), or by post-quantum cryptography, which is essentially a software based on a new generation of mathematical quantum algorithms.

In the nearest future as a development of this trend companies, working under such problem, will increase the number of qubits, improving the effectiveness at the same time. Also it should be noted that cloud access platform for quantum computers should be consonant with the other platforms, so we are going to witness synchronization of development processes in different countries.

Embedded finance and Open Banking

It's no surprise that many experts forecast the continued success of embedded finance in 2022. The rising demand for it has been a long time coming, so many financial institutions are increasingly offering banking as a service (BaaS). In order to make it real, online companies need new technologies and SDKs being available due to the fact that usually such services are distributed via opened APIs, also this trend would require strong antifraud and risk management measures to be taken.

Many experts say that a few previous years we have witnessed a lot of innovations in terms of fintech digital transformation. Indeed, remote work, new digital platforms and user experience somewhat confused a lot of users and led to certain limitation and problems. However it seems that 2022 is going to be more stable in terms of normal business activities. Innovation for innovation's sake no longer makes so much sense, a certain balance has been established and so we are going to see many changes in fintech in the nearest future.

Moreover, BNPL is also a part of such trend. Practically it is an alternative to credit cards, which lets the client to pay for purchases dividing payments. This allows trading platforms to become more accessible and providers can earn a percent from such payment or installment.

Money and technologies equal to a new start

A year gone by and speeded up the processes that many companies were trying to implement before and also shed light on some new problems.

Speaking of BNPL, not only the simplicity and speed of purchase are important for the end user, but also its safety. However, one of the main vulnerabilities of many BNPL companies is that they do not conduct official credit checks, using internal algorithms based on the information they have instead. The most effective way to solve this problem is device risk assessment and analysis of non-personal data, as well as the assessment of Internet connection and user behavioral data.

Apart from that, continuing the trend of non-personal data as a part of loan pipeline for neobanks and alternative lending, we offer the JuicyID product, which allows companies to strengthen the external perimeter of the client's personal account on the web portal or mobile application of a financial institution, identify a large set of dangerous device anomalies, highlight related devices of the same user, and, as a result, reduce losses. In addition, JuicyID can be effectively used as part of the protection of the personal account of creditors - the JuicyID data vector allows to build rules and models to protect financial and quasi-financial information, flexibly configure access authorization rules depending on the risk level of the device or user.

Machine learning methods are also a powerful tool that allows, with an understanding of the nature of the data and the correct application of modeling methods, to achieve practical solutions, such as predicting various kinds of risks. For example, JuicyScore is one of the most effective ways to increase the information value. We believe that it is necessary to strike a balance between secure, authorized access to data and the presence of a regulatory and methodological basis for the possibility of effective work of data consumers. When applying the regulation of data processing operations, a differentiated approach should be implemented, which would correlate with the level of risk for individual categories of data and the potential damage that may arise from malicious users.

Juicy Team will continue to maintain a high pace of development and delight our customers and partners with new product functionality, for you can ensure high competitiveness and business safety only through efficient and hard work in a dynamic digital world.